A secure home starts with a policy that shields money at tough moments. Clear wording avoids stress during claims so selection feels steady and calm. Coverage should fit your space size plus your belongings level for balance. Choose limits that reflect real costs so you avoid gaps during loss. Add options for special items when values rise past standard caps. Read exclusions with care so surprises do not appear later. Keep a simple inventory with photos or receipts to support payouts. Update details after new purchases or changes at home to keep protection aligned.

Core Coverage

Property insurance protects the structure plus the things you keep inside. The first subtitle also touches on Landlord Insurance as a related option when you lease a place. A standard plan usually includes fire plus smoke harm plus certain sudden water leaks. Most plans also include theft plus vandalism plus wind impact within set limits. Extra options can extend safety for electronics or art or jewelry. Always match deductibles to your savings so payments stay manageable during repair. Claims move faster when you keep documents ready plus contact details updated.

Home Hazards

Before the points below consider which sudden risks fit your home type and life stage. Use these notes to compare limits then select a plan that suits your needs.

- Fire damage coverage supports repair costs for walls floors roofs plus built fixtures.

- Smoke cleanup coverage helps restore interiors plus reduces extra living expenses after loss.

- Water leak events from burst pipes receive support when damage happens without neglect.

- ind storm harm may be covered for structure plus siding within policy terms.

- Theft events cover stolen items up to limits with proof like receipts or photos.

- Vandalism harm receives support for broken locks windows doors plus interior restoration tasks.

Policy Types

Choose between replacement cost or actual cash value for belongings. Replacement cost pays to buy new items at today prices without depreciation removal. Actual cash value pays after subtracting wear so payouts may feel smaller. Structure coverage can be open perils or named perils based on wording. Renters focus on belongings plus liability since the building belongs to the owner. Owners need structure coverage plus belongings plus liability for fuller protection. Review sublimits for cash jewelry art electronics since those caps affect payouts.

Personal Property

Use the short guide below to set strong limits for your belongings list. Adjust numbers after new purchases so the plan always mirrors current value.

- Make a room by room list covering furniture clothing electronics tools plus decor items.

- Record make model details where possible then store copies in secure cloud folders.

- Photograph serial numbers for key gear since that step speeds verification during claims.

- Add endorsements for jewelry art instruments or collectibles that exceed basic sublimits.

- Keep receipts or bank statements as backup proof for high value goods when needed.

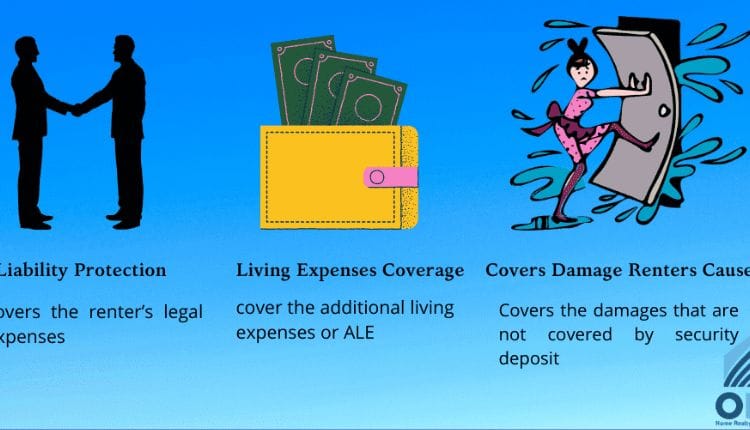

Liability Basics

Liability covers injury to others or harm to their items while at your place. It also helps with legal defense costs within stated limits inside the policy. Umbrella coverage can add higher limits across situations for extra peace of mind. Medical payments to others often handle minor injuries without proving fault. Choose limits that reflect your assets so one accident does not drain savings. Pets or certain features may change risk so disclose details to avoid denial.

Cost Factors

Use these notes to manage price without cutting essential protection you may need. Each step aims to bring steady savings with thoughtful choices in daily life.

- Higher deductibles lower premiums though you must keep cash ready for emergencies.

- Bundling home with another policy type can reduce bills within insurer rules.

- Safety devices like alarms locks sensors may unlock discounts after verification.

- Good claim history can support better rates at renewal with the same insurer.

- Credit based factors may influence price so maintain timely payments each month.

Smart Upgrades

These quick tips help strengthen your policy so support arrives without delay. Apply them during setup then check them at each renewal for freshness.

- Read exclusions carefully then ask for endorsements where you see coverage gaps today.

- Set loss of use limits to cover temporary stays if your home becomes unliveable.

- Add sewer backup coverage if local systems face occasional pressure or overflow risks.

- Schedule valuables separately so appraised items receive precise protection during claims.

- Review privacy rules with your insurer so documents remain secure across communications.

Strong coverage starts with clear goals then grows through careful choices over time. Match limits to true replacement values so you bridge costs during tough weeks. Keep records tidy for smoother claims since proof supports faster approval from teams. Add options where needed then review yearly because life details rarely stand still. Choose support from a stable provider who explains terms in simple language without jargon. A wise plan including Landlord Insurance where relevant helps to protect savings plus future plans.